Promising Markets For Cherries

Overview

Cherry is one of the highest-value stone fruits in international trade, selling at prices that are on average 3–4 times higher than peach, plum and apricot. Although cherries represent only around 19% of global stone fruit export volume, they account for about 46% of total trade value, making them particularly attractive for exporters targeting premium segments. Between 2020 and 2024, world import value grew from USD 3.929 billion to USD 6.426 billion, an increase of USD 2.497 billion. This translates into an average annual rise of about USD 624 million, showing strong expansion in global demand. For exporters, this highlights cherries as a dynamic and lucrative category with solid value growth potential, especially in markets willing to pay for quality, consistency and counter-seasonal supply.

Lebanon offers a wide assortment of fruits, nuts and vegetables with potential in high-end regional and European markets. Exporters of table grapes, avocados, citrus fruit and cherrieses often already handle a broader portfolio of fresh produce, which creates opportunities to diversify into additional high-value categories. In this context, cherries represent a promising product for Lebanese exporters. Although important value chain constraints still need to be addressed, the sector has clear potential to benefit from cherries as a premium crop with attractive market prospects.

Lebanon’s cherry exports remained unstable over the 2020–2024 period, reflecting both market and supply-side constraints. Export earnings increased from USD 1.339 million in 2020 to a peak of USD 4.532 million in 2021, before easing to USD 3.906 million in 2022 and dropping to USD 1.088 million in 2023. In 2024, exports recovered to USD 1.306 million, up 20% year-on-year, although still below the levels reached in the stronger export years. This performance indicates that cherries can be a valuable export product for Lebanon, but also highlights the need to improve consistency in production, quality, and market access to achieve more stable growth.

This report provides an overview of Lebanon’s current cherry production and export performance, its position in international markets, and the opportunities available to strengthen the country’s export potential, with the overall aim of enhancing the capacities and competitiveness of Lebanese exporters.

Product definition

Lebanon is among the notable producers of sweet cherries in the Mediterranean region and benefits from particularly favorable agro-climatic conditions for production. Cherries are cultivated at altitudes of 900–2,000 metres, which helps give the fruit its distinctive flavor, attractive color and firm texture. These characteristics support the positioning of Lebanese cherries as a premium product with export potential.

Where do Lebanese cherries currently go to?

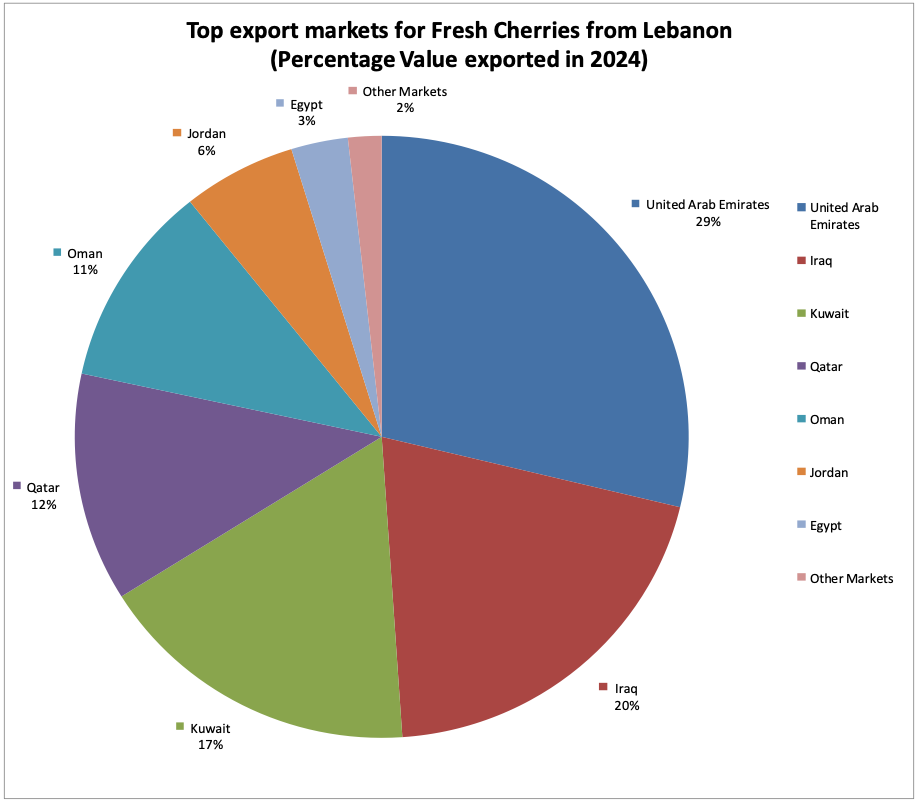

Together, the top five markets absorbed about 89% of Lebanon’s total cherry export value in 2024, highlighting the strong dependence of Lebanese cherry exports on a limited number of nearby regional markets.

Figure 1. Top export markets for cherries from Lebanon in 2024 - Source: ITC Trade map

What is Lebanon's position in the international market?

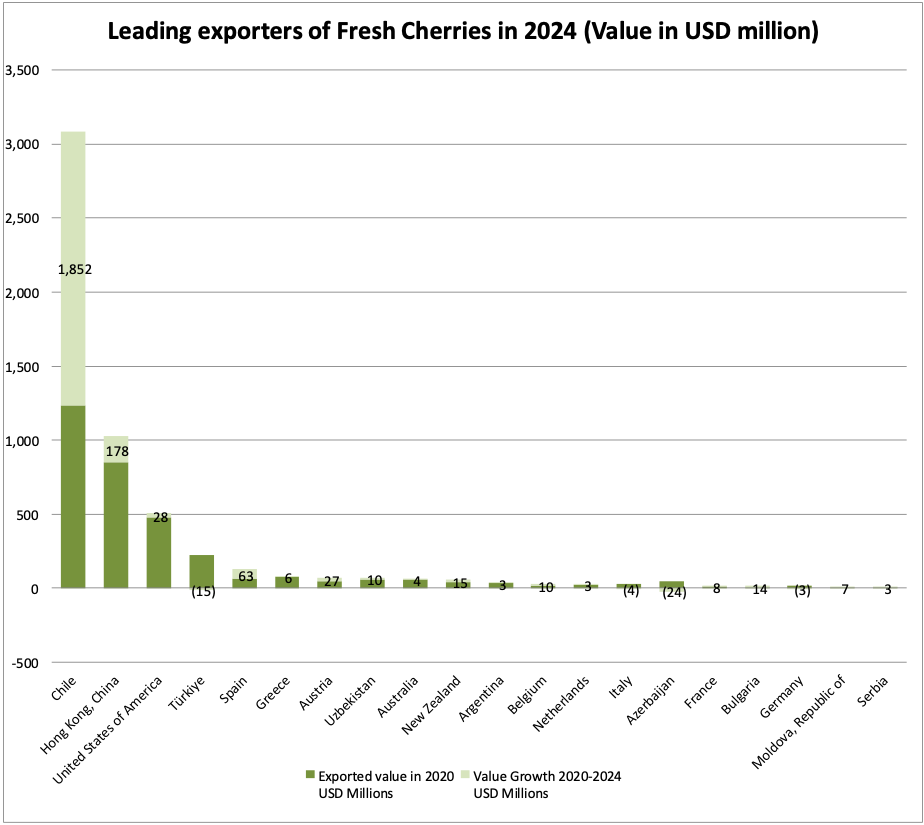

As shown in Figure 2, the largest exporters of fresh cherries worldwide in 2024 were Chile, Hong Kong, China, the United States, Türkiye, Spain, Greece and Austria. Chile dominated world exports with USD 3.087 billion, far ahead of Hong Kong, China with USD 1.027 billion and the United States with USD 506 million.

By comparison, Lebanon exported only USD 1.306 million of fresh cherries in 2024, placing it at about the 35th position among world exporters and confirming that it remains a very small player in global trade.

In competitive terms, Lebanon is more directly challenged by other suppliers from the Mediterranean region, especially Türkiye, Spain and Greece, which are well-established exporters in nearby and overlapping markets.

Largest Cherries Producers in the Mediterranean region

Within the Mediterranean region, the main cherry exporters in 2024 were Türkiye, Spain, Greece and Italy, with export values of USD 208.8 million, USD 129.2 million, USD 80.8 million and USD 25.7 million respectively.

Compared with these suppliers, Lebanon’s exports remained very limited. In competitive terms, Lebanon is therefore more directly challenged by these established Mediterranean exporters, especially Türkiye, Spain and Greece, which are active in nearby and overlapping markets.

As shown in Table 1 the supply season in Lebanon is between April and August. Lebanese cherries have strong domestic demand and have been exported for years to regional markets, where they still have growth potential.

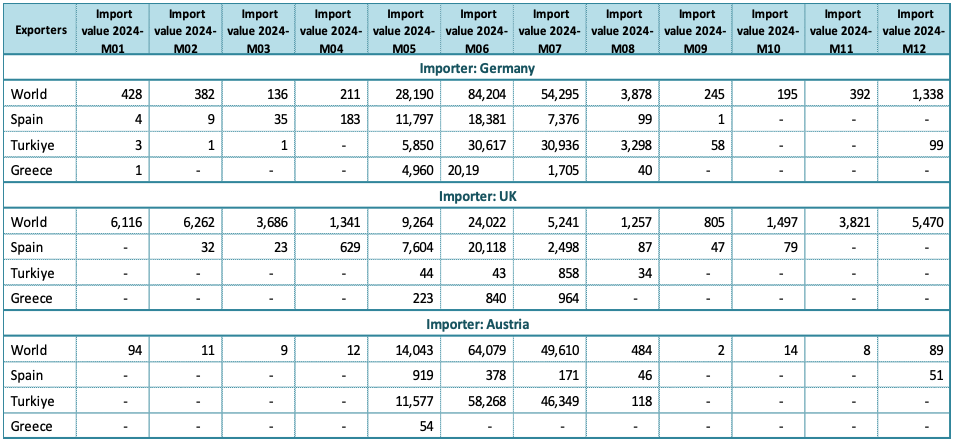

There is also an opportunity for high quality cherries in Europe, especially in the early season in May. The top regional cherries importers Germany, UK and Austria import the most between May and August as shown in Table 2.

Figure 2. Leading exporters for Cherries 2024 - Source: ITC Trade map

Table 1. Overview of cherries harvest windows in the world’s leading production countries

Table 2. List of supplying markets for a product imported by the most potential European markets in 2024

What are the trends in trade in the 20 largest importing countries?

The global fresh cherry market expanded strongly between 2020 and 2024. World import value increased from USD 3.929 billion in 2020 to USD 6.426 billion in 2024, confirming the strong growth momentum of international demand.

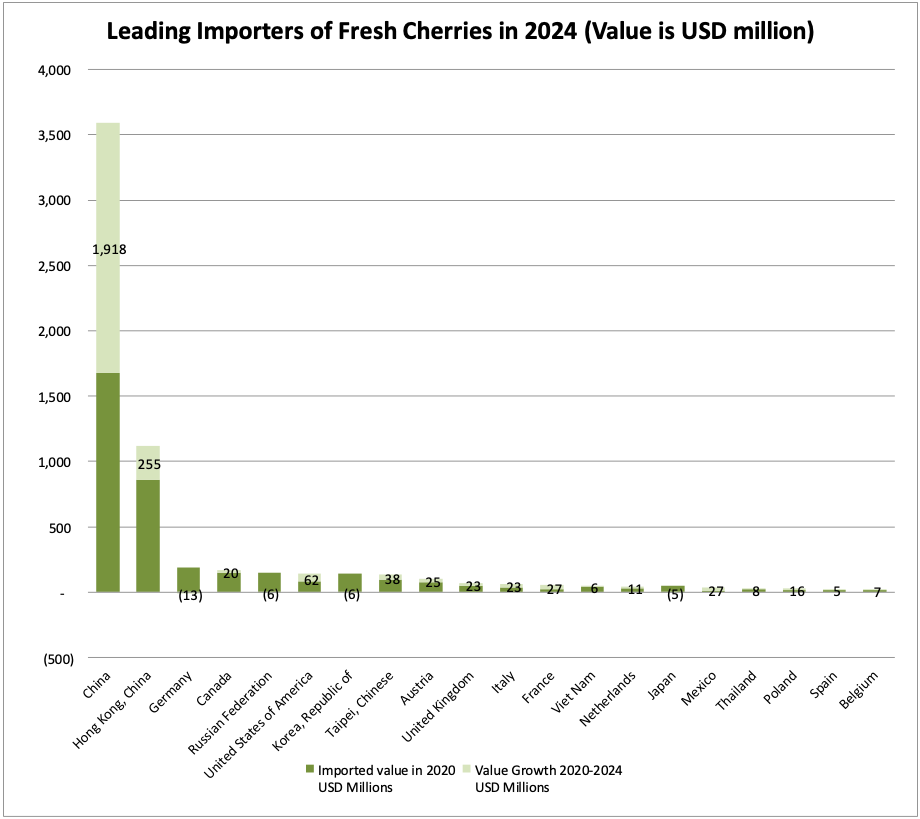

In 2024, China was by far the largest single market, with imports of USD 3.594 billion, equivalent to 55.9% of world imports, followed by Hong Kong, China with USD 1.117 billion or 17.4%. Other major importing markets included Germany, Canada, the Russian Federation, the United States, Korea and Taipei, Chinese.

For Lebanese exporters, this means that the largest global opportunities are concentrated in a few very large markets, although these are also highly competitive and already supplied by well-established exporters.

WHAT ARE THE TRENDS IN TRADE IN THE EUROPEAN MARKET?

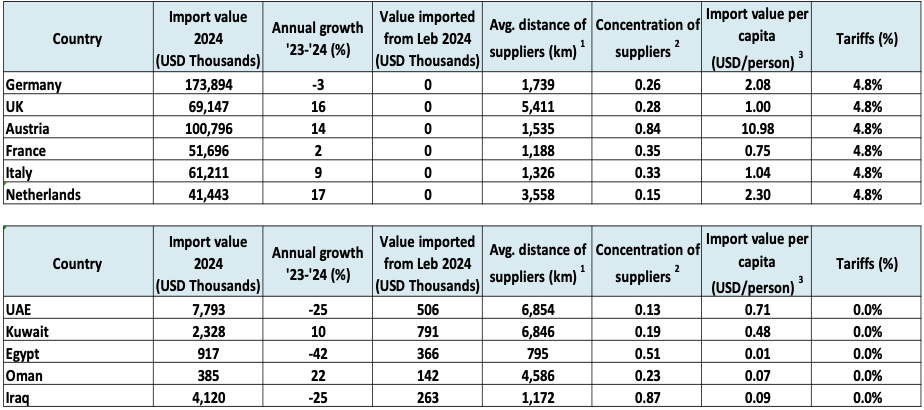

Europe remains an important destination for fresh cherries as a group of medium-sized but attractive markets. In 2024, the largest European importers were Germany (USD 173.9 million), Austria (USD 100.8 million), the United Kingdom (USD 69.1 million), Italy (USD 61.2 million), France (USD 51.7 million) and the Netherlands (USD 41.4 million).

Several European markets also recorded solid growth between 2020 and 2024, notably Poland (+20% per year), Italy (+17%), France (+14%), Spain (+11%) and Austria (+9%), while Germany remained broadly stable.

For Lebanese exporters, Europe therefore represents a diversified market with selective opportunities, especially in destinations that are growing and can reward quality supply, but it is also a more demanding market environment in terms of tariff and non-tariff requirements. In many EU markets, the estimated tariff is around 4.9% and the number of non-tariff requirements is 18.

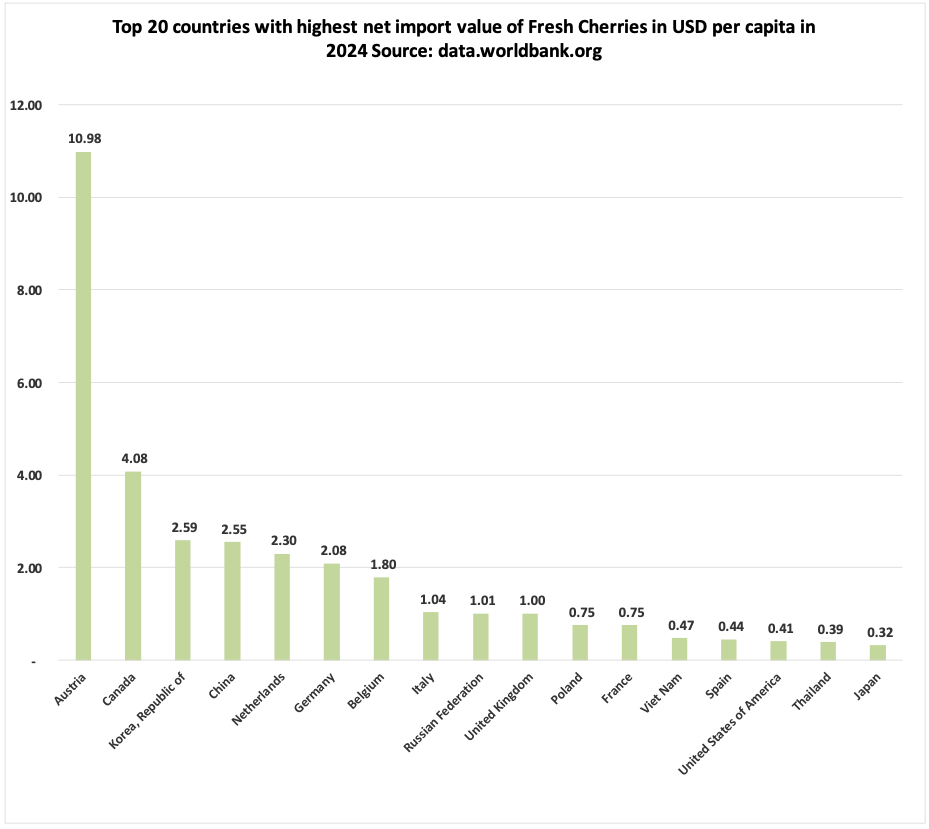

Figure 4 shows that Austria, Canada, Korea and China were the most import-intensive cherries markets per capita in 2024. For exporters, this points to established import demand and potentially attractive trade opportunities. Meanwhile, markets such as the Netherlands, Germany and Belgium, despite lower per capita import values, may offer room for future export growth.

WHAT ARE THE TRENDS IN TRADE IN THE GCC MARKET?

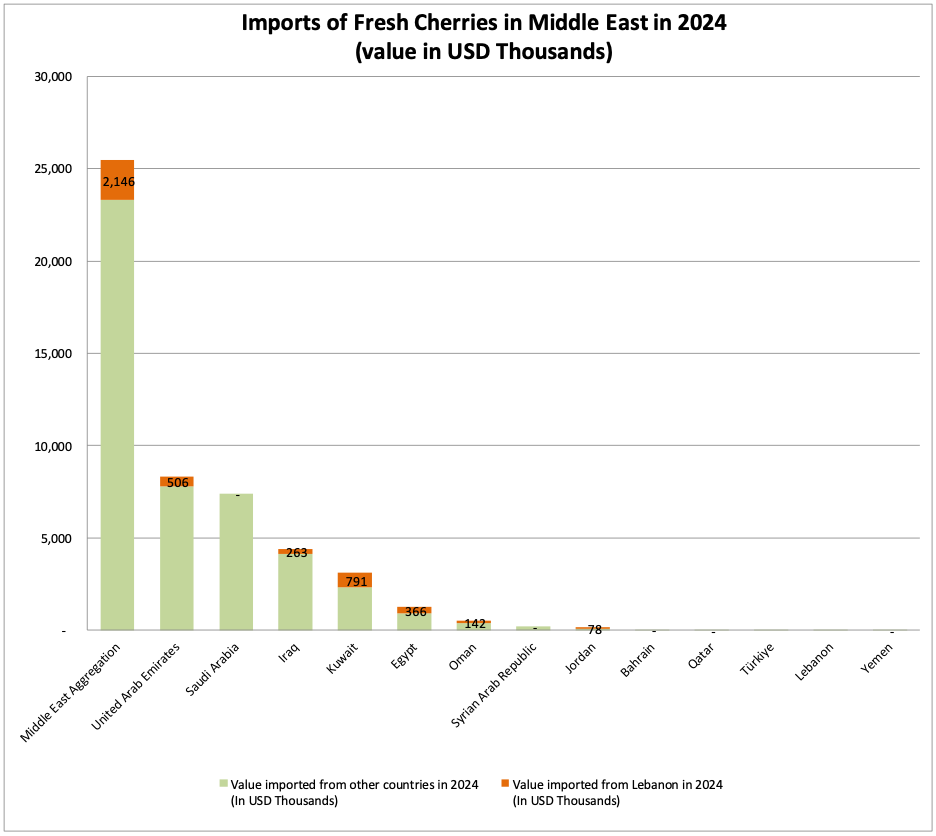

The GCC market is much smaller than East Asia or Europe, but it remains strategically important for Lebanon. In 2024, the largest GCC importers were the United Arab Emirates (USD 7.8 million) and Saudi Arabia (USD 7.4 million), followed by Kuwait (USD 2.3 million), Oman (USD 0.4 million), Bahrain (USD 32 thousand) and Qatar (USD 21 thousand).

Growth patterns differed across the region: the UAE showed very rapid growth between 2020 and 2024 (+146% per year) and Saudi Arabia also expanded strongly (+45% per year), while Kuwait declined over the same period (-16% per year).

For Lebanese exporters, these markets remain highly relevant because they are geographically closer, already familiar with regional fruit supply, and generally apply zero tariffs on cherries, although non-tariff requirements vary considerably from one market to another.

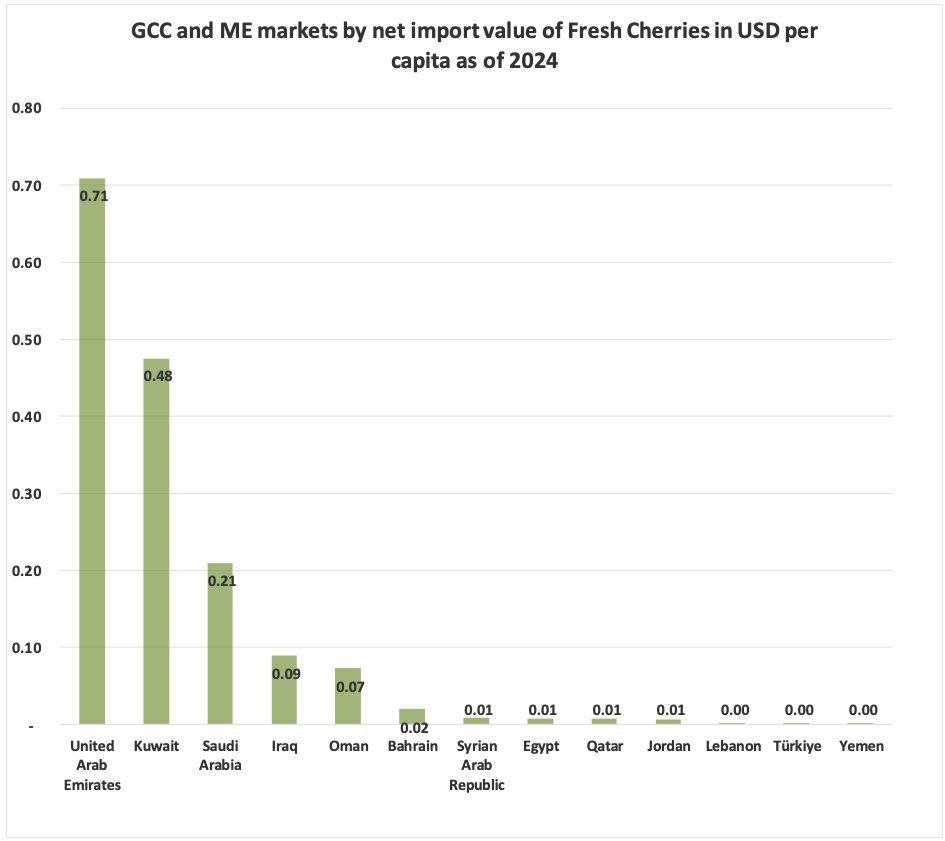

In terms of per capita consumption, the UAE and Kuwait stand out with more than twice the consumption of the other countries such as Saudi Arabia, Iraq and Oman. The Figure 6 shows there is still a lot of growth possible in many of the GCC and ME (Middle Eastern) markets.

For Lebanon, the most realistic export strategy is not to compete head-on in the very large Asian markets, where trade is dominated by major global suppliers, but rather to strengthen its position in regional Arab markets while selectively developing a presence in promising European destinations. Lebanon’s own fresh cherry exports reached only USD 1.306 million in 2024, compared with world exports of USD 5.573 billion, which underlines how small its current position is in global trade. At the same time, Lebanon faces direct competition from established Mediterranean exporters such as Türkiye (USD 208.8 million), Spain (USD 129.2 million) and Greece (USD 80.8 million). This suggests that Lebanese exporters should focus on markets where proximity, niche positioning and regional trade links can offer an advantage, particularly in the GCC and selected nearby or specialty markets in Europe.

Figure 3. Leading importers for cherries in 2024 - Source: ITC Trade map

Figure 4. Top 20 countries with highest net import value of cherries in USD per capita in 2024 - Source: ITC Trade map

Figure 5. Imports of cherries in Middle East in 2024 - Source: ITC Trade map

Figure 6. GCC and ME imports of cherries in USD per capita as of 2024 - Source: ITC Trade map

What are interesting markets for the future?

Short-term opportunities: nearby regional markets

The most practical short-term opportunities are in the UAE and Kuwait. The UAE imported USD 7.8 million in cherries in 2024 and already bought USD 506 thousand from Lebanon. Kuwait is smaller, at USD 2.3 million, but it grew by 10% and imported USD 791 thousand from Lebanon, the highest Lebanese export value among the shortlisted markets. Both countries apply 0% tariffs, buy from different suppliers, and are already familiar with Lebanese products. Oman may offer smaller niche opportunities, while Iraq is a larger market but harder to enter because supply is concentrated among a few suppliers. Egypt is currently a lower-priority market because imports declined sharply and import value per capita remains very low.

Medium-term opportunities: selected European markets

Europe offers much larger markets, but they are more demanding and should be seen as medium-term opportunities. Germany is the largest market in the shortlist, followed by Austria, the UK, Italy, France and the Netherlands. Among these, the UK and the Netherlands look especially interesting because they combine good growth with more diversified supplier bases. Italy also shows solid potential, while Germany remains attractive because of its size. Austria stands out for its high import value per capita, although entry may be harder because its supplier base is concentrated. Lebanon exported no cherries to these European markets in 2024, and all apply tariffs of around 4.8%, so entry will require careful preparation.

Why Europe is still difficult for Lebanon

Lebanon’s absence from these markets is not only a matter of competition. It also reflects practical constraints such as SPS readiness, cherry-fly compliance, certification gaps, weak cold-chain and post-harvest systems, logistics disruptions, and the fact that most Lebanese exports still go to easier regional markets. According to an interview with Lebanese exporter Mr Ghassan Feghali, competition in Europe is especially tough because Turkish suppliers are present in the same season and can ship by land, while Lebanese exporters often depend on air cargo, which raises costs. In addition, the Mediterranean fruit fly (medfly) issue is still pending with the Ministry of Agriculture, which continues to affect market access.

A possible entry window

Among the European markets, the UK may offer a practical entry window if Lebanese exporters can secure BRC certification and meet buyer requirements on food safety, traceability, phytosanitary compliance and cold-chain performance.

What this means for Lebanese exporters

In practical terms, Lebanese exporters should build first on the markets where they already have a foothold, especially the UAE and Kuwait, with Oman as a smaller additional option. Europe offers larger long-term potential, particularly in the UK, the Netherlands, Italy and Germany, but success there will depend less on price alone and more on consistent quality, reliable supply, strong post-harvest handling and full compliance with buyer requirements.

Table 3. Top potential markets for Lebanese cherries

Tips

- Start with the UAE and Kuwait. These are the most practical markets because Lebanon already exports there, tariffs are 0%, and buyers are familiar with Lebanese cherries. Oman can be treated as a smaller niche market.

- Treat Europe as a second step. Focus first on building stronger regional sales, then prepare for selective entry into markets such as the UK, the Netherlands, Italy and Germany.

- Compete on quality, not volume. Lebanon cannot compete with large suppliers such as Türkiye, Spain and Greece on scale. The better strategy is to offer good size, firmness, colour, presentation and reliable service.

- Strengthen post-harvest handling. Cherries are very sensitive, so fast cooling, careful handling, proper packaging and a reliable cold chain are essential to reduce losses and keep quality high.

- Prepare properly before targeting Europe. Exporters need stronger SPS readiness, fruit-fly compliance, certification, traceability and export documentation before approaching European buyers.

- Target the right market window. Lebanese cherries are most competitive when supply from main competitors is lower. Timing shipments well can improve prices and reduce direct competition.

- Work with the right buyers. Start with importers and traders who already handle premium fruit and understand the region, then build toward larger and more demanding programmes.